Independents, Private Equity, and Consolidators: Collision Repair Players and their Playbooks

Operators in the U.S. collision repair industry know there are many different kinds of players in the industry. Within one geographical area, there are collision repair enterprises with highly distinctive styles, reputations, work cultures, and owners. That’s how it’s always been, although the increasing complexity of cars in recent years has necessitated even more specialization by shops. What’s a relatively new dynamic is the rip-roaring pace of consolidation – either by regional rivals in a market or by the biggest names in the industry. Here at Focus Advisors, a mergers and acquisitions firm that focuses on collision repair, we often hear from owners, “so and so sold to Caliber” or “so and so signed up with CARSTAR.” And increasingly, we’re hearing, “this private equity firm gave me a call and offered me X. Do you know them?”

For some historical context, up until a few decades ago, the collision repair industry was comprised of many tens of thousands of one- to two-shop operations. Occasionally, there was larger enterprise than that – one of the early independent MSOs. Back in 2012, over 92% of collision repair locations throughout the US were doing less than $10M in annual sales, per the Romans Report. Those operators (sub-$10M in sales) comprised 32,500 shops across the US. By 2023, the number of enterprises doing less than $10M in annual sales declined by 23% to a count of 25,000.

A large part of this can be explained by the growth of the U.S. collision industry, which – during that same timeframe of 2012 to 2013 – grew from $30B per year to $50B per year. Cars became more advanced and costs went up, driving up annual sales per shop. However, the Romans Report also illustrates that most of the gains in the market size flowed to enterprises doing north of $20 M of sales annually. That means that the very large operators – those enterprises clearing upwards of $20 M in sales – gained significant market share in the last 13 years.

What these statistics demonstrate is that the collision industry has consolidated, and the large players are getting larger. We estimate that by the end of 2024, the largest operators had one-third of the collision repair market share. While there is still room for the small independent shops and independent MSOs to compete, they need to invest in management, techs, and specialization. They also need to know who the large players are and a little about their playbooks. This article will explore that.

The Whales and the Sharks of the Collision Repair Industry

In 2023, we here at Focus Advisors introduced the “Fish Scale,” which mapped out the various enterprises into different strata. At the top end of the fish scale are the “Whales” and the “Sharks.”

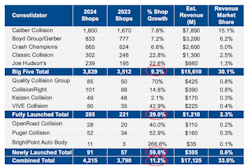

What we dubbed the “Whales” are the five largest collision repair consolidators, also known as “the Big Five.” In order of their market share, they are: Caliber, Gerber, Crash Champions, Classic Collision, and Joe Hudson's. Gerber is the lone public company among the consolidators; the remaining four are backed by private equity investors. These consolidators have grown their footprints through acquisitions, and increasingly, real estate developments in the last few years.

While the two smallest of the Big Five, Classic Collision and Joe Hudson's, grew by north of 22% in 2024, Caliber, Gerber, and Crash Champions grew by about a third of that pace. Collectively, at the end of 2024, the Big Five controlled 3,839 locations, comprising over $15.5 B of annual revenue.

Then there are the “Sharks.” These are smaller enterprises that have also been backed by private equity sponsors, although they are at an earlier stage of their maturation than the “Big Five.”

As background, private equity firms looking to enter the collision repair space will seek out an existing enterprise and entrepreneur with enough market share to form a “platform.” They will often pay a competitive price for this first platform, from which they will then launch a multi-year strategy of single-shop add-on acquisitions, often geography adjacent to their original platform. Over time, they will add shops through acquisitions, while also aiming those shops’ total sales and profit, as measured by EBITDA. After a few years, having grown total EBITDA, they then sell the enterprise — now substantially larger — to another buyer. This is a playbook that is otherwise known as a “roll-up.” It is behind private equity-backed consolidation in industries as diverse as HVAC and dental practices, and now to collision repair. It was what was behind the Big Five’s growth and now the seven “sharks.”

Leading the seven sharks is Quality Collision Group, backed by Susquehanna Capital. They grew their shop footprint by 35 locations, or 70% growth, in 2024. They closed on the two largest transactions in 2024 – that of Cascade, a nine-shop platform in Utah, and LaMettry’s, with 11 locations in Minneapolis. Their strategy is to focus on highly regarded local enterprises that have many OEM certifications.

Second to Quality Collision in terms of market share, there is CollisionRight, based in Dublin, Ohio. They were acquired by Summit Partners at the start of 2024, which gave them deep pockets to grow quickly throughout the year to a total of 101 locations.

Following CollisionRight is Kaizen (owned by Kinderhook) and VIVE Collision (owned by Greenbriar). They each closed the year with around 50 locations. Kaizen is located in several key markets on the west coast, whereas VIVE has come to be a driving force of consolidation in the Northeastern states.

The fifth shark is Puget Collision, which has expanded to over 52 locations throughout the Pacific Northwest. They have focused on acquiring franchise organizations through Driven Brands, such as Carstar and Fix Auto. They now have locations in Washington, Oregon, southern California, and Colorado. Collectively, these five largest “sharks” comprise almost $1.4 B in annual revenue, or 2.5% market share.

There are two more – OpenRoad and BrightPoint – which are much more nascent platforms, but which did see significant growth throughout 2024. All in all, there are seven “fully-launched collision repair platforms.”

Private Equity in Collision Repair

Given the background above, it’s clear that in recent years, there’s been a lot of talk about PE firms entering collision. Our firm, for instance, has been approached by over 130 PE firms looking to get a foothold in this industry. They’re attracted to industry’s resilience to recessionary pressures, its nature as a hedge against inflation, and its economies of scale across multiple locations, among other aspects. Many PE firms launched their platforms right around the time COVID started, as the Federal Reserve cut rates, capital was abundant, and the cost of capital was low.

But how did the low cost of capital translate to collision consolidation? Let’s start with the big picture. Private equity firms raise individual funds – getting capital commitments from institutional investors, family offices, accredited investors, et cetera. These investors are betting on the PE firm’s track record, but also their fund thesis, which commits to a certain strategy, risk/return profile, and target investment return over the course of the fund’s life cycle (typically around 10 years).

Once the capital is committed from those investors and the fund is “subscribed,” the PE firm immediately begins looking for investments to make based on its underlying thesis (while also charging management fees, I might add). Acquisitions they make are through a specific entity they create for that purpose and funded mostly with debt. In the case of collision repair, PE starts a new collision repair enterprise by paying up for a “platform,” a larger MSO acquisition, through which they typically keep the management on board to grow this platform to the next level in a few years. The goal here is to aggregate more sales and improve the profitability of the business. In four to seven years, they’ll aim to exit their investment and pay back their investors, so they hope to sell the enterprise to another PE firm – this time with more EBITDA and a higher EBITDA multiple.

This playbook has been executed several times since the collision industry began consolidating. Between November 2023 and May 2024, for instance, $9 B of capital came into the industry, providing the “Sharks” and the “Whales” with deeper pockets and mandates to grow – and grow fast.

While historically PE firms have looked for large platforms from which to launch, it became evident that those large transactions (let’s call them MSOs of at least six shops) were far and few between. When enterprises of that scale did transact, however, existing consolidators often had the leg up. So, being one of many dozen PE firms looking to get the deal was extremely competitive.

So starting in 2024, PE firms began approaching entrepreneurs much further upstream in the company life cycle, approaching energetic and capable collision entrepreneurs when they’re one- to three-shop enterprises. This became clear in November 2024, when TRP Capital launched a platform called Driving Force Collision by buying a three-shop MSO in Long Island, and Envest Capital Partners concurrently launched a platform called Authentic Auto Body by acquiring a single shop in Massachusetts.

These days, our firm hears of emerging platforms almost on a weekly basis, so this is a dynamic that is growing at a rapid clip.

Independents

While the Whales and the Sharks now control a third of the collision repair market share, that means two-thirds of the industry is still owned by independent collision repair providers. In the vast majority of cases, these are family-owned enterprises that have never raised outside capital. The “Independents,” as we like to call them, span an enormous range of sizes. Most independents are longstanding single-shop operations. But at the very top end, there are MSOs with over 20 locations. The largest independent MSO, by way of example, is G&C in Northern California, with 45 shops at the time of writing.

Each of these independent collision repair enterprises has a different business model. Some have DRPs in the enterprise’s DNA; others focus instead on OEM certifications. Some are franchisees with Driven Brands, for instance, and are able to scale that model well. There are some of the many ways independents have remained competitive in the face of significant consolidation. However, what’s become clear is that both cars and the collision repair industry are becoming increasingly sophisticated and require much more strategy on the part of owners.

For most owners, 2024 was a difficult year. Claims counts were down, and more of the cars that came into the shops were totaling. These headwinds really began in the second quarter of the year, and experts have cited many factors: a mild winter, economic uncertainty, an older car parc, or fear about getting dropped by an insurer for submitting a claim. Some of the larger independents, however, saw the down year as their opportunity to acquire at attractive prices. Texas Collision Group, G&C Auto Body, and Manders Collision and Glass are just three examples of independent MSOs that capitalized on the down-year by acquiring or even building new shops. There are many more.

Moving Forward into 2025

It’s critical to understand the composition of this industry and the different players within it. With only one public company in the entire industry (Gerber), there is still a lot of opacity in this industry, which makes it difficult to see how different enterprises are competing. What’s important to note, though, is that this is a growing industry, and two-thirds of it is still held by independent operators. Competition from consolidators and large independent players will intensify, especially as conditions normalize back toward pre-COVID levels. Operators looking to keep their footing in their markets must enhance: (i) enhance their understanding of their real-time financials, (ii) incentivize their management toward those financials, (iii) understand their valuation and its drivers, (iv) figure out ways to get repairable vehicles in the door at a consistent pace, (v) maintain their bench of technicians, and lastly, (vi) plan for growth. It’s a tall order. While more capital in the industry necessitates this, the good news is that it presents many new options for visionary collision entrepreneurs.

About Focus Advisors

Focus Advisors (www.focusadvisors.com) is the collision industry’s leading M&A advisory firm, partnering with MSOs between $10-100M in annual revenue, helping owners achieve maximum value through strategic growth and exits. Unlike traditional business brokers or large investment banks, Focus Advisors specializes exclusively in collision repair — giving owners unparalleled insight into value, interest, and opportunity timing. With over 25 years in the industry, Managing Director David Roberts has led more than 40 transactions totaling over $500 million in transaction value and more than 325 collision repair shops, including Tripp's Collision, Pride Auto Body, Quanz Auto Body, Mills Body Shops, and Master Collision Group. For a confidential discussion about your future, your value, and the benefits of having an experienced advisor on your side, visit our website or email Madeleine Roberts Rich at [email protected] or call (510) 414-7707.

Investment Banking Services and Securities offered through Independent Investment Bankers Corp. a broker-dealer, member FINRA/SIPC. Focus Advisors is not affiliated with Independent Investment Bankers Corp.

*Chart data and statistics on industry shop counts and acquisition volumes represent our best estimates from available public information, not statements of absolute fact.

About the Author

Madeleine Roberts Rich

Madeleine Roberts Rich is a Senior Associate at Focus Advisors Automotive M&A, the collision repair industry’s leading M&A advisor. Since joining Focus two years ago, she’s had the privilege of working with dozens of collision repair entrepreneurs in the US and Canada as they assess their growth or exit options.